What’s Behind Singapore Airlines’ Surprising Earnings Miss?

Singapore Airlines (SIA), widely regarded as Asia’s gold-standard flag carrier, just published its earnings for Q1 FY2025/26. Let’s go beyond the headlines and dissect what the numbers mean ...

Highlights

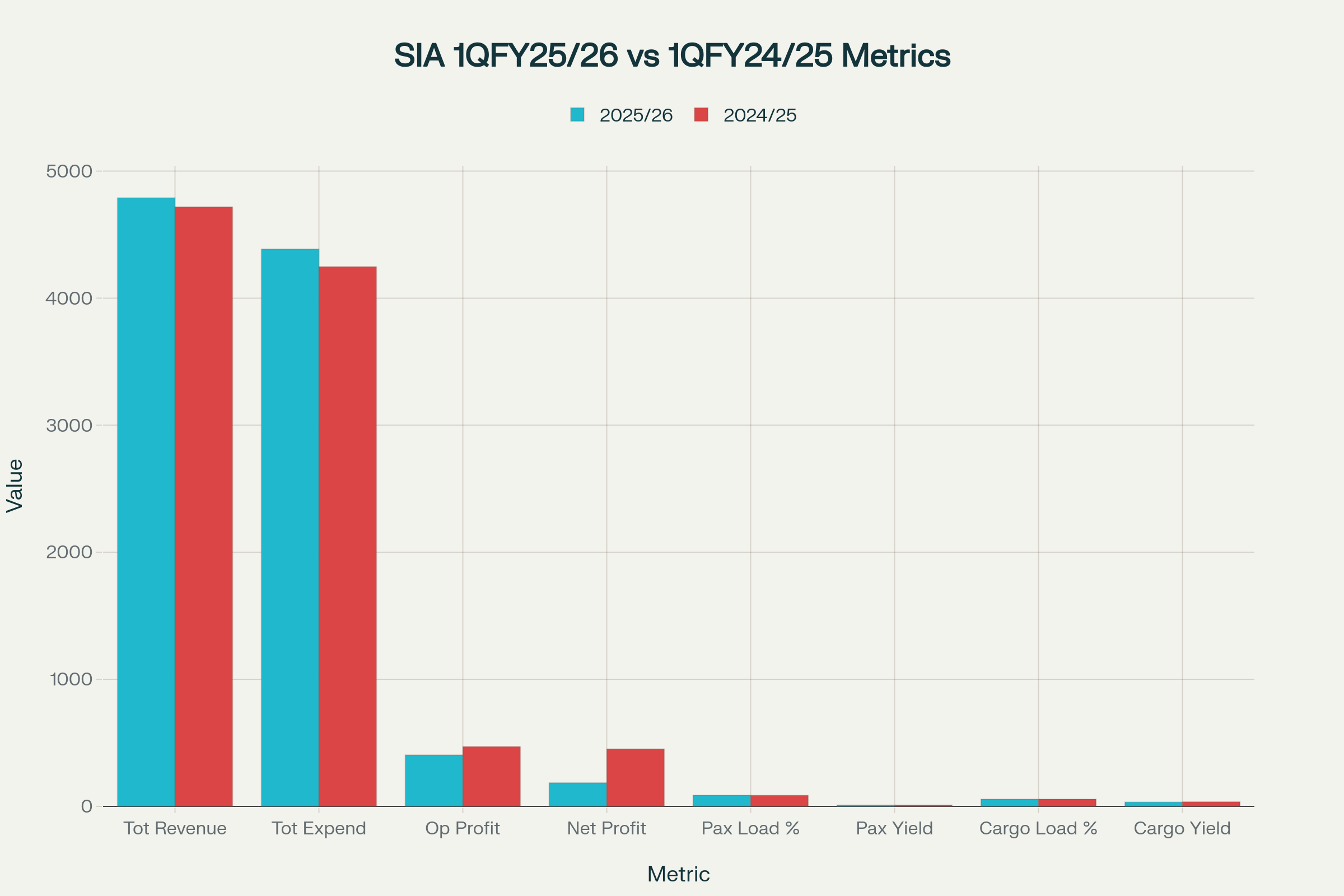

Net profit slid 58.8% to S$186 million compared to S$452 million last year, missing market expectations.

Total revenue up marginally by 1.5% to S$4.79 billion, thanks to record-high passenger traffic.

Earnings dragged down by Air India’s losses, lower interest income, and rising costs.

Shares tumbled up to 8.7% after the results—analysts downgraded the stock, flagging costly headwinds.

Balance sheet remains healthy with S$15.8 billion equity and debt/equity at 0.73.

Introduction

Singapore Airlines (SIA) has long sold itself as a fortress of quality, brand power, and prudent management in Asia’s competitive aviation landscape. But when the company posted its latest first-quarter results for FY2026, the numbers revealed that even industry champions are not immune to a “perfect storm” of industry normalization and unlucky investments. Let’s break down SIA’s latest update to understand what truly matters for shareholders and travelers alike.

Financial Results At a Glance

What Drove the Numbers?

Passenger Segment: Record Volumes, Falling Yields

SIA and Scoot carried a record 10.3 million passengers (+6.9% YoY), reflecting continued robust global flight demand even as international borders fully re-opened.

Group passenger load factor improved to a high 87.6%.

However, average yield dropped 2.9% as intense post-pandemic competition and capacity restoration by airlines worldwide forced SIA to price more aggressively.

Cargo Segment: The Boom Is Over

Cargo revenue dropped 1.9%, cargo yields slipped 4.4%—the once-hot freight market cooled as trade flows softened and bellyhold capacity flooded back into the system.

Cost Pressures Mount

Operating costs rose 3.2% YoY, mostly thanks to inflation, higher non-fuel expenses, and capacity expansions.

Net fuel costs were lower (-7.9%) due to cheaper oil, but the benefit was partially offset by higher flying volumes and a S$109 million fuel hedging loss.

Non-fuel expenditures surged 8.5%, outpacing revenue growth.

The Elephant in the Room: Air India Losses

The biggest “new” hit: SIA’s 25.1% stake in Air India, which pulled group net profit sharply lower. Air India’s heavy fallout from an integration- and incident-hit quarter led to associate losses exceeding S$120 million.

Lower interest income (–S$61 million YoY) also depressed the bottom line as SIA spent down cash and global rates fell.

Metrics

P/E Ratio: Currently 7.9x–8.6x for FY2026 vs. pre-pandemic average 18x. On paper, SIA appears relatively cheap, but uncertainty over earnings quality is high.

P/B Ratio: About 1.45x—statistically elevated, reflecting brand value and lingering optimism.

Dividend Yield: Approaching 6.5%, with a recent final dividend of 30 cents per share announced for FY2025.

Growth Prospects

Strong Brand and Network: SIA is aggressively expanding with 129 destinations across 37 countries, while Scoot adds new Asian routes in response to competitors’ exits.

Fleet Modernisation: SIA operates a young, fuel-efficient fleet (average age under 8 years), slated for further upgrades. 72 aircraft are on order.

Sustainability: Increased investment in sustainable aviation fuel and ongoing carbon reduction initiatives.

Air India Investment: Though painful now, integrating into the Indian market could be a needle-mover if Air India’s fortunes stabilize.

Premium Positioning and Partnerships: Joint ventures with Malaysia Airlines and others increase integrated offerings, premium market access, and scale benefits.

Risks and Headwinds

Air India Losses: Major short-term risk. Losses are expected to widen before any possible turnaround, with high execution and reputation risks.

Yield and Margins: As more airlines ramp up service and capacity globally, SIA will face difficulty defending its pricing premium, especially as cost inflation persists.

Cargo Weakness: Freight remains oversupplied amid weak global trade, pressuring cargo yields and margins.

Geopolitical and Macroeconomic Volatility: Potential shocks (trade, fuel, interest rates, travel disruptions) weigh on management’s cautious optimism.

Valuation Richness: Elevated P/B and relatively low forward earnings visibility argue for risk moderation.

Conclusion

SIA remains a world-class operator, but the FY2026 first-quarter results are a timely reminder that even the best-run airlines operate within a turbulent context. Air India is now a double-edged sword for SIA: a big drag today, but a potential long-term lever if restructured successfully. Passenger demand, especially for premium services, is still strong—but price and cost pressures are likely to keep margins in check.

For investors, the outlook is muddied: valuation is optically attractive, but downside risks are not trivial. Expect ongoing market volatility, muted earnings, and a likely period of adjustment as the group absorbs associate losses, adapts cost structures, and beds down its strategic bets in India and Southeast Asia.

For travelers, healthy competition and SIA’s premium standards mean more network options and consistently high service offerings, even as fare bargains become harder to find.

Sign up now and get our free REITs’ Numerical Ratings.

Disclaimer: This article constitutes the author’s personal views and is for entertainment and educational purposes only. It is not to be construed as financial advice in any form. Please do your own research and seek advice from a qualified financial advisor. From time to time, I have positions in all or some of the mentioned stocks when publishing this article. This is a disclosure - not a recommendation to buy or sell stocks.