🗓️ Weekly Market Update

📊 What’s Happening?

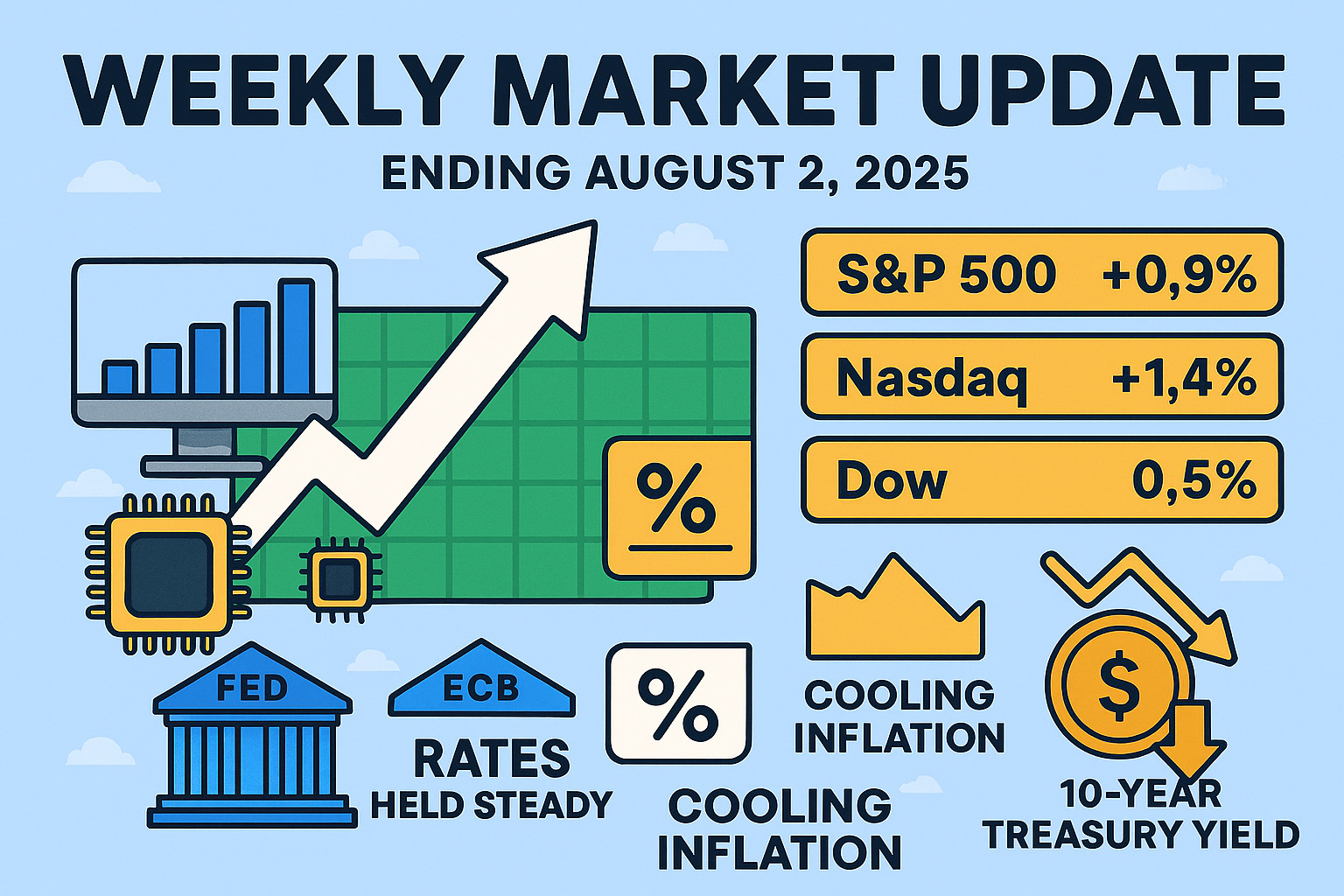

Wall Street wrapped up the week with a mix of relief and caution. The focus was sharply on earnings season, central bank signals, and economic data. The S&P 500 edged higher, up 0.9% for the week, and the Nasdaq saw a 1.4% gain, helped by strong tech earnings. The Dow Jones Industrial Average posted modest gains as well, registering its fifth consecutive weekly win.

On the macro front, the Federal Reserve and the European Central Bank both kept rates steady, but with a noticeably more cautious tone. This shift stirred speculation that rate cuts could come as early as Q4 2025, especially with recent data showing cooling inflation and sluggish job growth.

📉 Why Does It Matter?

This week’s developments highlighted a few key themes:

Big Tech surprised to the upside: Alphabet (Google’s parent company) crushed earnings expectations and announced a $80 billion tech spending, sparking a rally in the tech sector. Apple and Amazon also soothed investor nerves with better-than-feared results.

Economic moderation gaining traction: The latest US GDP report showed growth slowing to 1.8% annualized in Q2, a sign that higher interest rates are finally biting. Meanwhile, the PCE (Personal Consumption Expenditures) inflation index came in soft, adding fuel to the easing narrative.

Bond yields slipped, echoing market sentiment that central banks may pivot sooner than expected. The 10-year Treasury yield fell to 4.15%, the lowest since May.

Markets are starting to price in a reality where the Fed cuts rates in December, a timeline previously seen as too optimistic.

💡 Opportunity

Investors are now balancing earnings resilience with macro uncertainty. With signs pointing to a cooling economy but not a hard landing, growth stocks—especially in tech—remain in favor. Companies with strong cash flows, capital return programs, and pricing power stand out.

If the Fed begins to talk more openly about pivoting, we could see a renewed rally in rate-sensitive sectors like real estate, fintech, and biotech. On the fixed income side, bond investors may want to consider locking in yields before rates head materially lower.

As we head into August, watch for further guidance updates, consumer confidence numbers, and geopolitical headlines—all of which could sway investor sentiment quickly.

🧠 TL;DR

This week gave bulls something to smile about: Tech earnings crushed it, growth is slowing but not crashing, and central banks are dropping taper hints. Markets may continue drifting higher—as long as inflation behaves and policy doesn’t tighten further. Keep your eyes on the Fed speak and economic data as indicators for the next move.

Sign up now and get our free REITs’ Numerical Ratings.

Disclaimer: This article constitutes the author’s personal views and is for entertainment and educational purposes only. It is not to be construed as financial advice in any form. Please do your own research and seek advice from a qualified financial advisor. From time to time, I have positions in all or some of the mentioned stocks when publishing this article. This is a disclosure - not a recommendation to buy or sell stocks.